PRYSMIAN CONTINUES GROWTH AND MARGIN EXPANSION IN Q4’25 2025 IS PRYSMIAN’S BEST YEAR YET

- PRYSMIAN CLOSES FY25 WITH ITS HIGHEST-EVER ADJUSTED EBITDA (€2,398 MILLION), NET INCOME (€1,270 MILLION) AND CASH GENERATION (€1,171 MILLION)

- CONTINUED ORGANIC GROWTH (+4.3%) AND PROFITABILITY1 ENHANCEMENT (14.5% VS. 12.7%, Q4’24) IN Q4

- TRANSMISSION Q4 MARGIN IS BEST-IN-CLASS (20.9% VS. 14.5%, Q4’24) AND COMPLEMENTED BY ORGANIC GROWTH (+8.4%). BACKLOG AT €17 BILLION

- POWER GRID ORGANIC GROWTH ACCELERATION IN Q4 (+12.8%), DRIVEN BY NORTH AMERICA & EMEA

- ELECTRIFICATION: INDUSTRIAL & CONSTRUCTION REGISTERS ORGANIC GROWTH (+0.6%) AND GROWING MARGINS (13.5% VS. 12.9%, Q4’24) IN Q4, DRIVEN BY DATA CENTER EXPANSION IN NORTH AMERICA

- DIGITAL SOLUTIONS ADJUSTED EBITDA NEARLY DOUBLES IN Q4 (€75 MILLION VS. €40 MILLION, Q4’24), INCLUDING THE STRONG CONTRIBUTION FROM CHANNELL. REVENUES UP (+8.4% ORGANIC GROWTH)

- FREE CASH FLOW BEATS FY25 GUIDANCE AT €1.171 MILLION (+15.8% VS. FY24)

- FURTHER CONSISTENT PROGRESS ACROSS ALL SUSTAINABILITY KPIs, INCLUDING 50% OF EMPLOYEES AS SHAREHOLDERS – ACHIEVING THE 2028 TARGET THREE YEARS IN ADVANCE – AND SCOPE 1 & 2 GHG EMISSION REDUCTION AT 40.2% VS. 2019 BASELINE (37.0%, FY24)

- INNOVATION: SUSTAINABILITY-LINKED REVENUES RISE TO 44.2% (43.1%, FY24)

- CASH RETURN TO SHAREHOLDERS: PROPOSED DIVIDEND TO INCREASE 13% TO €0.90

- FY 2026 OUTLOOK DRIVEN BY A POSITIVE CONTRIBUTION FROM ALL BUSINESSES

- Adjusted EBITDA expected in the range of €2,625 to €2,775 million

- Free Cash Flow expected in the range of €1,300 to €1,400 million

- Sustainability-linked Revenues expected in the range of 47 to 49 percent of total Group Revenues

Massimo Battaini, Prysmian CEO, said: “This outstanding year is another milestone, and represents the start of a new chapter of growth and profitability. The excellent fourth quarter, and the first year of our ‘Accelerating Growth’ strategic plan, underlines that we are proceeding on the path to meet our mid-term targets. From our acquisition of Channell, to the successful integration of Encore Wire, Prysmian has once again demonstrated its track record of successfully incorporating value-generating M&A, accelerating the strategic evolution to world-class solutions provider. Building on this, the leadership position of our Transmission business will be further enhanced thanks to the agreements to acquire Xtera and ACSM. At the same time, our financial solidity is demonstrated by our strong free cash flow, which is well ahead of guidance. Our achievements in 2025 were also underpinned by our ambition to introduce new sustainability-driven solutions to accelerate organic growth, reduce carbon emissions and increase the circularity of our business. The continued value creation over the past year is made even more special because 50% of our employees are now shareholders. Their passion, their innovations, their team spirit and sense of belonging will propel us even further in the years ahead.”

Milan, February 26, 2026 – The Board of Directors of Prysmian S.p.A. has approved the Group’s consolidated results for 20255.

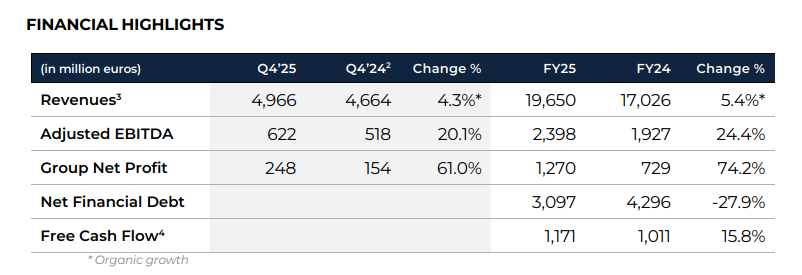

Group Revenues in the fourth quarter stood at €4,966 million, up from €4,664 million in Q4’24 with +4.3% organic growth. There was continued robust organic growth in Transmission (+8.4%), Power Grid (+12.8%) and Digital Solutions (+8.4%). In Electrification, organic growth was +0.6% in Industrial & Construction, while Specialties contracted (-2.1%).

In FY25, Revenues reached €19,650 million (€17,026 million, FY24), with +5.4% organic growth.

Revenues reflect the inclusion of both Encore Wire, which was fully consolidated as of July 1, 2024, and Channell, fully consolidated as of June 1, 2025.

Adjusted EBITDA in Q4’25 reached €622 million, up 20.1% compared to €518 million in Q4’24. The overall margin at standard metal prices was 14.5%, up from 12.7% in Q4’24.

In the fourth quarter, Transmission’s Adjusted EBITDA rose significantly to €181 million (€119 million, Q4’24), as did the margin, reaching a best-in-class 20.9% (14.5%, Q4’24).

In Power Grid, the Adjusted EBITDA was €105 million (€117 million, Q4’24), and the margin was 12.1% (15.4%, Q4’24). The margin was temporarily impacted by a surge in metal premiums in the Overhead Transmission Line business.

In Electrification, the Adjusted EBITDA in Industrial & Construction was €202 million (€185 million, Q4’24), and the margin improved to 13.5%, up from 12.9% in Q4’24. In Specialties, the Adjusted EBITDA was €61 million (€59 million, Q4’24), while the margin rose to 10.4% (9.6%, Q4’24).

Digital Solutions saw continued profitability expansion, with the Adjusted EBITDA almost doubling to €75 million (€40 million, Q4’24). The margin increased significantly to 18.3% (13.2%, Q4’24), thanks in part to the contribution from Channell.

In FY25, the Adjusted EBITDA was €2,398 million (€1,927 million, FY24) and the margin was 14.2%, up from 12.9% in FY24.

EBITDA increased in FY25 to €2,688 million (€1,754 million, FY24).

Group Net Profit in FY25 was Prysmian’s highest ever, reaching €1,270 million compared with €729 million in FY24, thanks in part to a gain (€346 million net of tax) from the sale of the stake in YOFC.

Free Cash Flow was €1,171 million, an increase compared with €1,011 million in FY24, and ahead of the FY25 guidance.

MEDIA & INVESTOR RELATIONS

Maria Cristina Bifulco

Chief Strategy, IR, M&A and Communication Officer

- phone-

- email[email protected]

media relations

Jonathan Heywood

Communication, Public Affairs & Media Relations Director

- phone+39.331.6573546

- email[email protected]